As President Bola Tinubu’s administration celebrates one year in office, the first quarter (Q1) 2024 real Gross Domestic Product (GDP) growth report calls for stock-taking, resetting of some ineffective economic policies, and weeding out non-performing ones to enhance speedy revitalisation of the struggling economy, writes JOSEPH INOKOTONG.

Nigeria’s economy appears to have defied all the odds with its current performance in retrogression despite numerous measures by the government to stimulate growth. The odds seem stacked against a quick retreat to progression, and it is not very likely that remarkable and inclusive growth will beckon anytime soon.

Already in April, the inflation rate soared to 33.69 percent, relative to the March 2024 rate which was 33.20 percent, according to a report by the National Bureau of Statistics (NBS). Looking at the movement, the April headline inflation rate showed an increase of 0.49 percent points when compared to the March 2024 rate.

The NBS reported that the food inflation rate in April 2024 was 40.53 percent on a year-on-year basis, which was 15.92 percent points higher compared to the 24.61 percent rate recorded in April 2023. It attributed the rise to increases in prices of items like Millet flour, Garri, Bread, Wheat Flour prepacked, Semovita (which are under Bread and Cereals Class), Yam Tuber, Water Yam, cocoyam (under Potatoes, Yam and other Tubers Class), Coconut Oil, Palm Kernel Oil, Vegetable Oil, etc (under Oil and fat), Dried Fish Sadine, Catfish Dried, Mudfish Dried (under Fish class), Beef Head, Beef Feet, Liver, Frozen Chicken (under Meat class), Mongo, Banana, Grapefruit (under Fruit Class), Lipton Tea, Bournvita, Milo (under Coffee, Tea and Cocoa Class).

When the Central Bank of Nigeria (CBN’s) Monetary Policy Committee (MPC), last week continued its tightening posture by raising the Monetary Policy Rate (MPR) by 150 basis points to 26.25 percent from 24.75 percent, the Organised Private Sector (OPS) raised the alarm. They cautioned that the persistent high depreciation value of the Naira will continue to feed inflation, while constraining firms’ investments and household consumption. Consequently, they reasoned that raising the policy rate will further exacerbate inflationary pressure as growths in factory costs and commodity prices become unbounded.

Economic experts had opted for a hold position because in their views, the aggressive policy rate hike is taking a toll on output, and production is stifled because of the very high cost of funds. Moreover, they submitted that the seeming overreliance on the MPR as a tool to tame inflation does not appear to be making any meaningful impact due to the significant non-monetary factors driving inflation in Nigeria such as the high cost of energy, transport as well as insecurity in the food-belt regions of the country.

However, Mr Olayemi Cardoso, Governor of the Central Bank of Nigeria (CBN) rose in stout defense of the hike in interest rate, reiterating that the key focus of the CBN remains to achieve price stability, using monetary policy tools to rein in inflation. He informed that the past tightening stance of the Bank has started yielding positive results.

Interestingly, Nigeria’s Gross Domestic Product (GDP) data released by the NBS at the weekend seems to align with the position taken by the economic experts; output fell below the previous record.

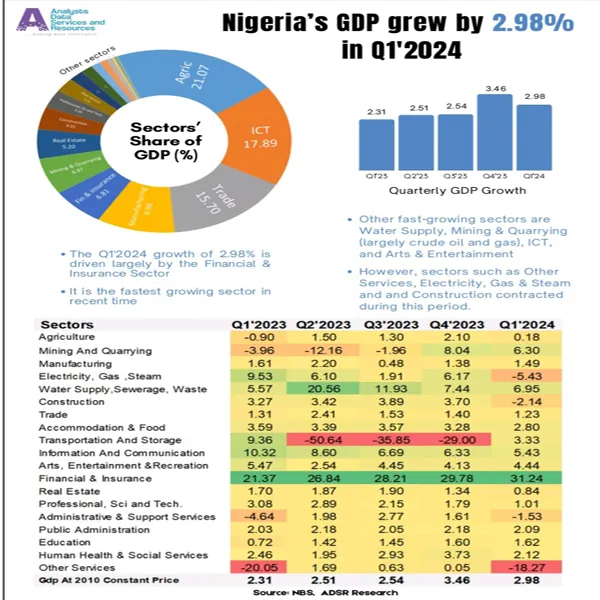

According to the NBS, Nigeria’s Gross Domestic Product (GDP) grew by 2.98 percent (year-on-year) in real terms in the first quarter (Q1) of 2024. This growth rate is lower than the 3.46 percent recorded in Q4 2023 but higher than the 2.31 percent achieved in Q1 2023.

The performance of the GDP in the first quarter of 2024 was driven mainly by the Services sector, which recorded a growth of 4.32 percent and contributed 58.04 percent to the aggregate GDP.

The agriculture sector grew by 0.18 percent, from -0.90 percent recorded in the first quarter of 2023, while the industry sector growth was 2.19 percent, showing an improvement from 0.31 percent achieved in the first quarter of 2023.

In terms of share of the GDP, the services sector contributed more to the aggregate GDP in the first quarter of 2024 compared to the corresponding quarter of 2023.

Also, the country recorded an average daily oil production of 1.57 million barrels per day (mb/d) in the first quarter of 2024, which was 0.06 mb/d higher than the 1.51 mb/d recorded in the same quarter of 2023 and 0.02 mb/d higher than the 1.55 mb/d production volume recorded in the fourth quarter of 2023.

The non-oil sector grew by 2.80 percent in real terms during the reference quarter (Q1 2024). This rate was higher by 0.02 percent compared to the rate recorded in the same quarter of 2023 and 0.28 percent points lower than the fourth quarter of 2023.

This sector was driven in the first quarter of 2024 mainly by Financial and Insurance (Financial Institutions), Information and Communication (Telecommunications), Agriculture (Crop production), Trade, and Manufacturing (Food, Beverage, and Tobacco), accounting for positive GDP growth.

The top contributing sectors to GDP in Q1, 2024, include Agriculture 21.07 percent, ICT 17.89 percent, Trade 15.70 percent, Manufacturing 9.98 percent, Finance & Insurance 6.81 percent, Crude oil 6.38 percent, and Real Estate 5.20 percent.

Experts attribute the lackluster performance of the Q1 2024 GDP to the aggressive hike in the monetary policy rate of the CBN in February 2024, which they had cautioned against.

Commenting on the Q1 2024 real GDP performance, Professor UchennaUwaleke, Director, Institute of Capital Market Studies, Nasarawa State University Keffi said the growth pattern, which is weighted in favour of the services sector, is not healthy for a developing economy such as Nigeria’s.

Professor Uwaleke stated, “I note the following regarding the Q1 2024 real GDP performance: The aggressive hike in monetary policy rate by the CBN in February 2024 hurt output in Q1 2024.

“Just like in Q4 2023, when growth was driven by the oil sector, growth in Q1 2024 was also driven by the oil sector at 5.70 percent. Oil sector growth was aided partly by the increase in crude oil production during the quarter (from 1.55mbpd in the previous quarter to 1.57mb/d).

“The Non-oil sector performance was powered by the Services sector chiefly financial services and ICT.

“Manufacturing and agriculture sectors appeared hugely impacted by economic headwinds during the quarter. Growth rates were a mere 1.49 percent and 0.18 percent respectively.

“The Agriculture sector (comprising 4 activities although dominated by crop production) tanked significantly in Q1 2024 to 0.18 percent from 2.10 percent in the previous quarter. With the agricultural sector’s dismal performance, it is easy to understand why food inflation has climbed to over 40 percent as of April 2024.

“The financial sector grew by 31.24 percent, a clear demonstration that it is detached from the productive sectors of the economy.

“In my view, this identified growth pattern, weighted in favour of the services sector, is not healthy for a developing economy such as ours. Little wonder, economic growth does not appear inclusive reflecting in rising unemployment and poverty levels.

“It is time we reset this faulty economic structure, leveraging technology, in favour of the productive sectors: Industry and Agriculture. Indeed, structural change is strongly recommended (by UNCTAD) as one of the ingredients of building productive capacities.

“The Economy is Tanking: MPC should pause policy rate hike.”

The projections for the nation’s economy paint an optimistic trajectory as the Federal Government of Nigeria anticipates real GDP growth of 3.76 percent in 2024, slightly surpassing the estimated 3.75 percent for 2023. This optimism is underpinned by implementing key government reforms to shape the economic landscape. Foremost among the factors contributing to this positive outlook is the expectation of improved crude oil prices and production, highlighting the crucial role the oil industry is expected to play in driving economic growth.

As President Bola Tinubu’s administration celebrates one year in office, it is pertinent to take a second look at economic policies initiated to weed out ineffective ones to enhance the speedy reinvigoration of the struggling economy. Leapfrogging the economy on the inclusive growth trajectory requires policy re-evaluation as the Q1 2024 real GDP figure suggests that the economy is tanking. Experts advise the government to target double-digit real GDP to stem the rising unemployment and create an enabling environment for businesses to thrive.

ALSO READ: Workers’ welfare: Ibadan poly staff unions demand Oyo govt’s immediate action

WATCH TOP VIDEOS FROM NIGERIAN TRIBUNE TV

- Let’s Talk About SELF-AWARENESS

- Is Your Confidence Mistaken for Pride? Let’s talk about it

- Is Etiquette About Perfection…Or Just Not Being Rude?

- Top Psychologist Reveal 3 Signs You’re Struggling With Imposter Syndrome

- Do You Pick Up Work-Related Calls at Midnight or Never? Let’s Talk About Boundaries